View on payment industry modernisation: Drivers of change

Industry Leader, Financial Services and Consumer, EMEA

Let's start engineering impact together

GlobalLogic provides unique experience and expertise at the intersection of data, design, and engineering.

Get in touchThe post-pandemic era has accelerated these efforts as consumer behaviour changed significantly during the COVID-19 outbreak. Consumers across the world expect real-time responses in all aspects of digital payment transactions and have adopted digital behaviours, paving the way for cashless economies.

The modernisation is both revolutionary as well as evolutionary – it covers almost every aspect of the payment ecosystem.

According to 2021 paper, modernisation of the payment ecosystem has enabled payment transactions to generate roughly 90% of useful customer data – this is turn is shifting people away from the old-fashioned perspective of payments being an operational activity only.

In fact, digital payments are becoming more strategic. And businesses looking to meet their customers’ expectations will need to invest in refining their digital experiences at every point in their digital journey, starting with payments.

Let’s dive into the details…

So, what’s driving change in the payment industry?

1. Cashless economy

Before the pandemic, we all knew that the use of cash would deteriorate over time, leaving countries that rely on cash to grow slower economically. Some countries have taken drastic measures, such as demonetisation, to shift consumer behaviour over to digital transactions in order to boost the economy.

Fast forward to the present day and the use of cash is declining in favour of digital payments. And as consumers become more confident with digital payments, countries and financial institutions are encouraging cashless societies as they bring transparency to payment systems; ultimately reducing fraudulent activity.

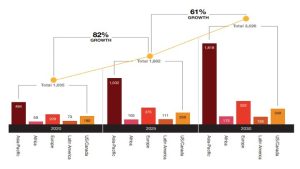

According to analysis by PWC, global cashless payment volumes are set to increase by more than 80% from 2020 to 2025 – from about 1tn transactions to almost 1.9tn, and to almost triple by 2030.

Figure 1: Number of cashless transactions in billions. Source: PWC

According to figure 1, Asia-Pacific is anticipated to grow the fastest, with cashless transaction volume increasing by 109% from 2020 to 2025, and then by 76% from 2025 to 2030; followed by Africa (78%, 64%), Europe (64%, 39%) and Latin America (52%, 48%). It’s suggested the US and Canada will have the least rapid growth (43%, 35%). But these cashless transaction totals for 2025 and 2030 are just projections.

In short, cashless transactions are becoming the norm, and research shows it’s not just good for the consumer. BCG research anticipates that countries that are digital could boost annual GDP by as much as 3%.

2. Availability to pay 24/7

With the mobile and cloud era upon us, 24/7 self-service has become a common perk in most financial institutions. Nowadays, fulfilling consumer demand for services are delivered quickly, easily and 24/7. With a fast-paced life and the rise of an ‘always-on’ culture, consumers want payment whenever, wherever, to whoever, and however they want (usually through one of many channels – including smart phone, tablet, and the web).

Financial institutions and businesses need to be ready to meet the 24/7 self-service availability level of expectation in the payment initiation area – this remains critical to the overall customer experience.

3. Instant Payment/Real-Time Payments (RTP)

With advancements in technical infrastructure and an overreliance on instant gratification, consumers expect payments to be instant. Instant payments or RTPs are electronic payments that are processed in real time – 24 hours a day, 365 days a year – where the funds are made available immediately for use by the recipient.

RTPs have spread quickly in recent years due to increased demand. Consumers expect cleared funds in their bank account immediately and access to funds as soon as they are available – which is far more efficient than payment by check or waiting for funds to clear through an automated clearing house or even same day payment.

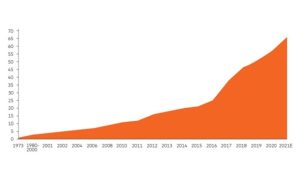

The global RTP market size is currently valued at $17bn and is expected to reach $193bn by 2030, growing at a compound annual growth rate (CAGR) of 34.9% from 2022 to 2030, as per a 2022 EY report. The predicted growth can be substantiated by the fact that deployments of RTP are at an all-time high.

Figure 2: Number of live real-time systems. Source: Mastercard

RTP systems present businesses with the opportunity to engage and retain their customers through new, more efficient, secure, and engaging services – these systems typically support always-on environments. The speed of the payment combined with the certainty that accompanies irrevocability means they are well suited for creating new possibilities.

RTP operators are overseeing the creation of rules and standards for new overlay services that will help realise increased benefits for end-users and, most importantly, act as a catalyst for greater and wider innovation.

Overlay services – such as request to pay, instant cross-border payments, biller directory, fraud prevention services, customer directory etc. – are common offerings which build on infrastructure to deliver enhanced value to the participants of a payment network. Organisations leveraging payment networks have the opportunity to create new business use cases on top of overlays services for increased customer experience.

4. Seamless and secure payment

The modern-day consumer is demanding. They expect convenience and security when interacting with businesses – especially when it comes to their personal information, card details, and payment data. For example, 30-35% of customers drop from merchant sites after they start the payment check out process – purchasing becomes a frustrating experience due to registration of payment information on multiple sites while at checkout.

Businesses need to standardise and offer secure communication on all channels consumers use to do payment transactions. Both convenience and security matter for new age consumers, rather than having a choice between the two.

To conclude:

Industry transformation is influenced by multiple factors – from government policies to social changes, business trends to advancement of technology. We may think of payment modernisation as being a top-down approach instigated by the government, public bodies, and central banks that drive policies, but the trends that are really driving change in payment industry are dominated by social changes – such as consumer expectations, societies becoming more affluent, and increasing demand of hyper-personal experience.

Businesses must keep a sharp focus on their customers’ needs and continue evolving whilst providing new propositions.

How?

The payment industry has been adapting social changes to modernise its ecosystem. Businesses must leverage these enablers to provide new and innovative services that solve pain points or offer tangible benefits to their customers.

First step you can take to leveraging these enablers: contacting us to find out how we can help.

About the author:

Manik Jandial has over 22 years of experience in the software industry and specialises in new product development. He possesses a deep passion for leading product teams, guiding them from the ideation and discovery phase to the build and delivery phase.

Manik’s expertise extends across technology, program, and product management, enabling him to consistently deliver value-driven products for our customers. He has a diverse product development background spanning the telecom and B2C domains, with experience at organisations like Samsung R&D.

In recent years, he has concentrated on the payment domain, creating products and services for a prominent global technology payment organisation. His expertise includes real-time and card-based payment ecosystems, new payment methods, digital wallets, P2P and bill payment services, as well as ISO 20022 / ISO 8583 payment messages.

Prior to transitioning into product and program management, Manik gained extensive programming experience in languages such as C, C++, and Java. He holds a bachelor’s degree in engineering, a postgraduate certificate in General Management, and certifications like Project Management Professional (PMP) and ScrumMaster (CSM). Manik actively pursues continuous learning in product management, regularly participating in courses and staying updated with industry trends.